Streaming, gaming, gambling, and social media used to be in their own lanes – different companies, different regulators, different audiences. A few years ago, things started to get blurry between all four. Today, all four live on the same device, follow the same evening schedules, and use the same tricks to keep us engaged – personalized feeds, time-based nudges, loyalty rewards.

The UK is a great place to look at all this in motion – the market is mature enough to be interesting, the data is publicly available, and the regulator publishes detailed numbers. So here’s a look at how things are positioned, how they intersect, and what might be next.

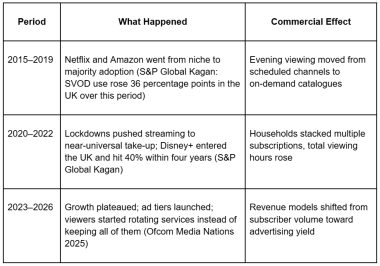

Streaming After the Growth Phase

The subscriber rush is over. Netflix reached roughly 70% of UK internet households by the end of 2024, Amazon Prime Video sat at 59%, and Disney+ at 40%, according to S&P Global Kagan’s European Consumer Insights survey. Overall SVOD take-up plateaued at around 85% that year – the same level as 2023.

Ad Tiers and the New Revenue Split

Ad-supported plans arrived across Netflix, Disney+, and Amazon in 2023–2024. For plenty of users, these became the default – cheaper and tolerable enough. Ofcom’s Media Nations 2025 report confirmed that broadcaster content still accounts for most in-home viewing when you measure across all delivery methods. The shift across the past decade happened in three stages:

Global platforms still hold a structural edge because they can spread production costs across dozens of markets. British content is strong. Whether British platforms can hold onto it – or whether it ends up wherever the licensing cheque is biggest – is the open question.

Gaming, Gambling, and the Overlap Between Them

Over half of UK internet adults play video games, a figure that held flat for five years (S&P Global Kagan, December 2024 survey). Mobile gaming takes 55% of revenue (Market Data Forecast, UK Gaming Market 2025). The two industries share more plumbing than they appear to:

- Both depend on mobile-first delivery – gaming through app stores, gambling through licensed casino online platforms, and betting apps.

- Both use algorithmic personalisation to recommend content, adjust difficulty or odds, and time notifications to individual habits.

- Both monetise through upfront payments, in-app purchases, and subscription tiers mixed together.

- The casino bonus model – deposit incentives, free spins, loyalty tiers – works on the same logic as the battle pass and season pass mechanics that gaming studios use to hold players.

Both industries cater to global customers via localized apps and regional payments. The African countries are seeing rapid growth in mobile entertainment in South East Asia, and emerging markets are growing rapidly in mobile entertainment, powered by young populations and low-cost smartphones. Platforms like play at Win Casino in Bangladesh show how operators adapt their products for specific regional markets. The UK, with its detailed regulatory framework, often works as the testing ground – what gets approved or restricted here shapes product roadmaps in dozens of other countries.

The AI Layer Across Everything

Ofcom’s Online Nations 2025 report recorded 1.8 billion UK visits to ChatGPT between January and August 2025, up from 368 million in the same months of 2024. Gemini grew 146% year-on-year over the same period, Claude 138% (Ofcom Online Nations 2025). Around 30% of search queries now return an AI-generated overview before any traditional links.

AI does not sit in its own category. It runs through every other one:

- Streaming: Netflix’s recommendation engine drives most of what people watch; Spotify’s Discover Weekly does the same for audio.

- Gaming: studios use AI for procedural content, dynamic difficulty, and NPC behaviour – it shapes the experience without most players noticing.

- Gambling: the Win casino online model relies on algorithmic personalisation to suggest games, adjust interfaces, and time promotional alerts to individual patterns.

- Social media: feeds are entirely AI-curated, which decides what entertainment content – including ads and marketing – reaches any given user.

AI cuts the friction between wanting something and finding it. That helps every platform with a deep library and a decent recommendation engine. It hurts anything that depends on active searching or scheduled discovery, which partly explains why traditional TV and radio keep losing ground.

What the Next Three Years Probably Look Like

Predicting exact outcomes is a bad bet. Directions are clearer:

- Streaming revenue will lean harder on advertising, with subscriber-only plans becoming a premium tier rather than the norm.

- Gaming will widen its audience as cloud services remove the need for expensive hardware – older users and lower-income households are the growth pool.

- Online gambling will keep moving from shops to phones, with regulators tightening affordability and marketing rules further.

- AI will go deeper into content discovery, production, and personalisation across every entertainment sector.

British adults have roughly the same free time they had ten years ago. The number of products engineered to fill those hours has multiplied. The ones that hold attention longest – by reducing the gap between opening an app and finding something worth staying for – will take the largest share of the money. That is the competitive logic now, and it applies equally to a streaming service, a mobile game, and an online casino online platform.

This is a submitted article